Debt fund enhances the overall value of the portfolio, if chosen properly. Debt funds offer variety of products that are based on different time horizon to meet individual investment needs. Selecting a debt fund is a tougher task then selecting an equity scheme. Below given are some of the important points that are to be kept in mind before making the selection. Investment time horizon Investors should first be aware of their future cash flow requirement before making the fund selection. Investors should define the period for which they want to invest.

Short maturity funds include Liquid, Ultra short term & short term funds.

Medium maturity funds include corporate bond and credit opportunities fund.

Long maturity funds consist of Income, Gilt & dynamic bond funds.

Portfolio Indicators Yield to Maturity (YTM) is the expected yield that the portfolio will generate from the coupon payments if the securities are held till maturity. Average Maturity is the weighted average maturity of all the securities held in the portfolio. Higher the average maturity, more sensitive is the portfolio to the interest rate movement. Modified Duration is a measure of sensitivity of the price of a bond to change in interest rates. If modified duration of the portfolio is 3 years and interest rates goes down by 1%, then Net Asset Value (NAV) of the fund will go up by 3 per cent. Higher the modified duration, higher will be the sensitivity of the price for a given change in interest rate. Allocation to Credit rating Credit rating indicates the credit risk that the fund assumes. Debt funds tend to invest in securities having varied credit ratings. Portfolio consisting of sovereign & higher rated papers implies lower default risk. Higher the credit rating of the securities in the portfolio, safer will be the investments. Allocation to different asset classes Debt funds invests in the various instruments like government bonds, state government bonds, corporate bonds, PSU bonds, treasury bills, cash etc. issued by different entities. Government bonds are more sensitive to movement in interest rates compared to corporate & PSU bonds. Cash and current asset in the portfolio ensures availability of funds to meet day to day redemptions from the fund. Market Scenario See to it where the interest rates are expected to move in the overall economy – upwards or downwards for near term as well as few years down the line. When interest rate cycle is in an uptrend, it makes sense to invest in short term debt funds, while in a falling interest rate scenario invest in longer duration debt funds. Other than above, one should also look at the investment objective of the scheme, performance track record over a period of time vis-a vis its benchmark & other fund features like corpus and exit load.

Indians are ready for retirement, but haven’t saved enough. Survey, Aegon Retirement Readiness Survey 2015, reveals that approximate 73% of the respondent form the India believed that they will have to support family members, apart from spouse or partner, financially after retirement.

The person aged 35 today and having the monthly expense of Rs 25000/- wanting to retire at age 55 and life expectance of 80 years will require the approx 3.13 Cr rupees only for the retirement considering 8% inflation and 9% rate of return post retirement. His monthly household expense would be Rs 1,16,524/- which is currently Rs 25000/-.

The best time to start investing for your retirement is the day you get your first pay check. But it is always better to start late than never.SIP (Systematic Investment Plan) through the Equity Mutual Fund is the best Investment strategy for investing for the Retirement.

It is very essential to know the right amount of the fund you will require and the monthly investment you are required to do for attaining the peaceful Retirement Life.

SIP has a power to deliver the better return than the traditional Recurring Deposits in a long run. As on 30th June, 2015 the Average return given by SIP in Equity Funds for 15 years of period is 20.24%, while the minimum return was 13.11% which is far higher than the return from the recurring deposit of any bank or post office.

Ø Have you planned for your retirement enough?

Ø Do you know what would be your monthly house hold expense at the time of your retirement?

Ø Do you know the pace at which your expenses will increase post retirement?

Ø Do you know how much corpus you need to accumulate to live a peaceful retirement Life.

Click Here to know how much retirement corpus you will need and the SIP amount required to achieve that corpus.

Congratulations on making it through to another tax season! Have you ever thought why most people tend to wake up in the month of March to save tax? This is, because they consider tax planning as one-time ritual that will help them from paying taxes. All they want is to get the maximum possible income tax benefits.

Tax planning is not something you should wait till the end of the financial year; it’s something you should start early and build on it.

Tax planning should always be considered as a part of your overall financial plan. While tax saving is important, investments made for this purpose will also help you move closer to your financial goals.

If you start your tax planning early, you can…

Avoid the risk of locking your funds in an unsuitable product

Have lesser burden at the end of the financial year as investments get spread over 12 months

Achieve your financial goals

Follow the below given Steps for optimizing your Tax Planning:

Determine your Tax Liability – Calculate the amount of tax liability and the amount of deduction you want to claim based on the estimates of your income for the financial year

Determine the amount of Fresh investments you need to make – Evaluate whether your current investment towards tax planning will be sufficient enough to meet the amount of deduction you require.

Choose the right Instrument

If you don’t have sufficient life cover buy a term life insurance

Adequate Health insurance cover is equally important as it takes care of your physical and financial health during a medical contingency.

Important things to be kept in mind while selecting tax saving instrument for investments:

- Goals

- Risk appetite

- Lock in period

- Inflation

- Taxability of Income

- Your personal Tax slab

Conclusion Tax planning should ideally begin at the start of every financial year. Remember, the risks of planning tax-saving in a hurry later are manifold.

The Indian youth never had it so good. On the consumption side, the choice of goods & services available is unprecedented. And as far as income is concerned, given the blooming economy & its ever improving prospects, opportunities have ever been better! So, the youth is earning a lot & spending a lot! It’s definitely a happy situation to be in!

As a college student, you should be focusing on your financial future as well as your studies. No, not the financial future consisting of next week’s pizza fund, but your long-term personal financial future. Make sure you start your life after studies on the right financial foot by treating your financial future seriously while you’re still in college.

Young investors have an edge over others on account of their age. In other words, a young investor has more time on hand as compared to middle-aged investor or one who is nearing retirement. Young investor can take higher risk compared to middle aged investor or nearing retirement investor. This in turn affords young investors greater flexibility while making investment decisions.

If we take simple example, most of the young spend Rs. 500 per month very easily on food, entertainment, etc, how much money they are losing in future, is illustrated with the help of power of compounding method.

Power of compounding

Years

12% return p.a.

15% return p.a.

0-5

Rs. 40,835

Rs. 44,287

6-10

Rs. 1,15,019

Rs. 1,37,609

11-15

Rs. 2,49,790

Rs. 3,34,253

16-20

Rs. 4,94,628

Rs. 7,48,620

21-25

Rs. 9,39,423

Rs. 16,21,765

26-30

Rs. 17,47,482

Rs. 34,61,640

(Assume the individual invests Rs. 500 per month.)

The percentage of younger generation in India is more compared to old. Over the past couple of years Indian economy has seen unprecedented economic boom leaving more surplus money in the hands of people. The young can use financial planning route to meet their future financial goals. They have their whole lives ahead of them, and ample time to plan for every goal including retirement. The problem with the masses is that they do not plan for their finances. Some who have a decent salary packages and decent amount of surplus available also invest without doing proper asset allocation in various asset classes like equity, debt, real estate, gold, etc.

There are various investment avenues available to young investors and the various facets of each avenue like small saving schemes, equity, mutual funds, ELSS, unit linked insurance plan, etc. Today youth should ensure that he is associated with the right investment advisor at all times. He could well be the individual who plugs the gap between youth achieving or not achieving his financial goals and objectives. Financial markets have become very complex and there are varieties of products available to choose from. The choice of product will depend upon:

Age of the client

Time horizon of investments

Risk appetite of investor

Need of the investor

As a rule of thumb, a person shall invest % of his portfolio in debt equal to his age and the remaining amount in equity after providing for sufficient amount in the form of liquid assets / cash for emergency provision. A person shall also plan for the purchase of residential house. A young person has a high risk appetite and the time horizon of investments is also long, he should invest more money in equity and equity related instruments and fewer amounts in debt. When a person starts working, his income level is also low and there is very less surplus available for investments after meeting his monthly expenses. Every young person would like to become rich very fast.

The small amount of saving per month if done in a disciplined manner and systematically will lead to a higher amount of wealth accumulation over a longer period of time. If a young person of age 23 starts saving Rs. 2,000 per month till he is age 60, he will be able to accumulate Rs. 3,96,06,204, if rate of return on investments is 15% p.a. In this case I have not taken into consideration the increase in salary and thus increase in amount of investments.

The young investors have to first do their asset allocation. After deciding about asset allocation, the choice of products will start.

These financial tenets shall never change or become irrelevant. Follow them if you want to protect your finances against uncertainty.

Have a plan, be rich

This is, perhaps, one virtue that can neutralise the impact of various financial sins. A plan acts as a guide through your financial journey and, even if domestic and global upheavals dent your investments, it will help you get back on track. At the macro level, planning affects every aspect of personal finance, be it taxation, insurance or achievement of goals.

It can cut losses, enhance gains, and avoid the pain and panic of a financial or lifestage crisis. At another level, a plan is a simple matter of listing out your needs and wants, and deploying the money in right avenues so that you have it when you need it. As a first step, calculate your existing worth and identify the goals for which you will require money in the future. Calculate the exact amount required for each goal after factoring in inflation and the time horizon in which you want it. ..

Find out your risk-taking ability and then pick the instruments you want to invest in (asset allocation). Link your investments to goals and you won't have to scrounge around for money when you need it. Build a plan the minute you are employed because you can invest without straining your finances and without the burden of responsibilities.

More importantly, it will help you gain from the power of compounding. So if you wake up to the need of a retirement kitty at 40, you're likely to save much less than if you started at 25 (see graphic). It is likely that your planning will go for a toss in a market collapse like that of 2008, but will typically stand you in good stead through most ups and downs.

Secure your family & finances

Most people are so intent on investing and building assets that they forget to cover their risks. Since it's crucial to secure your family and finances by creating an adequate insurance portfolio, this is the second constant that does not change with time. A majority of the people buy insurance to save tax and as an investment, with life insurance the second most favoured investment destination after fixed deposits, accounting for 25% of wealth of small investor.

Never ignore taxes

Much like death, taxes will never go away. While rules and slabs may change from time to time, taxation itself won't. In fact, it affects every aspect of your finances, from income and allowances to investments as well as the assets you buy or sell. So, stop ignoring or pushing it away.

Monitor your investments

Creating a plan and building a portfolio may go to waste if you do not monitor it periodically. A review is essential to mark the progress towards your goals and take corrective measures, if required. As critical as a medical check-up, you should monitor the investments on a quarterly basis for short-term goals, and annually for long-term goals. While some people display undue exuberance, checking twice a week or more, it is prudent to do it at longer intervals. In changing market conditions, an important thing to analyse is the asset allocation, which could have changed and will need to be rebalanced.

Selling something that is doing well and buying into a losing asset class might appear counter-intuitive, but in the medium and long term, a portfolio based on asset allocation has a better chance of outperforming the market. Next, one must look at individual performances of investments and remove the funds or stocks that have not performed consistently for more than four quarters.

Be aware, stay alert

The more things change, the more this rule holds. A good financial plan not only means investing in the right avenues and monitoring the plan's progress, but also ensuring that you don't lose your hard-earned money to frauds, identity theft and sheer ignorance. Financial knowledge and caution can translate into higher gains and fewer losses for you in any market condition.

You can start by taking note of the various fees and charges that are straining your budget and reducing your savings. Whether it's credit card usage or travel planning, banking or realty transations, make sure you don't give away more than you should. Next, ensure you don't invest in an instrument you know nothing about, especially when it comes to stock investments.

Endowment policies, by their very nature, are difficult to understand. For instance, if you have bought a wrong policy and want to weed it out from your portfolio, it's not easy to calculate how much money you will get. Let's understand how to do that.

If you stop paying premium before the end of the policy term, you are entitled to receive an amount, called surrender value, depending on the number of years completed, the premium and the bonus received.

There are two types of surrender value-guaranteed surrender value and special/cash surrender value. While the guaranteed value is easy to calculate and is mentioned in the product brochure and the policy bond, the special surrender value is calculated only after the policyholder puts in the surrender request.

GUARANTEED SURRENDER VALUE:

You are eligible to receive this if you have paid premium for at least three years. It is 30 per cent of the basic premiums paid, excluding the firstyear premium. Additional premium for riders such as accidental death benefit is excluded.

If you have paid Rs 75,000 (Rs 25,000 annually for sum assured of Rs 5,00,000) in the first three years, the minimum you will get is 30 per cent of Rs 50,000 (total premium paid minus first-year premium), that is, Rs 15,000.

This does not include the bonus that you may have received from the insurer. If your policy pays bonus, which you accrue during its term, the amount you will receive on premature closure (surrender) of the policy will be the special surrender value.

SPECIAL OR CASH SURRENDER VALUE:

Before special surrender value, we must understand paid-up value. If you stop paying premium after a specified period, your policy will continue but with lower sum assured. This reduced sum assured is called paid-up value or paid-up sum assured.

Paid-up value is calculated by multiplying the original sum assured and the ratio of the number of premiums paid to the number of premiums payable.

Let us consider that you pay the Rs 25,000 annual premium on a quarterly basis, and the sum assured is Rs 5 lakh for a policy term of 20 years. If you stop paying after three years, that is, have paid 12 premiums, the paid-up value will be Rs 5,00,000X(12/80).

Special surrender value = {Basic Sum Assured X (Number of Premiums Paid/Total Number of Premiums Payable) plus total bonus received}X Surrender Value Factor.

Earlier, we calculated the paid-up value as Rs 75,000. Assuming that the bonus is Rs 60,000 and the surrender value factor in the 3rd year is 27.76 per cent, then the special surrender value = 27.76 per cent (Rs 75,000+Rs 60,000) = Rs 34,476.

In this case, 80 (20X4) is the number of premiums you were supposed to pay and 12 (3X4) is the number of premiums you have actually paid.

The paid-up value is Rs 75,000. This is the sum you will get at maturity or your nominee will get after you die. Paid-up value plus bonus is the total paid-up value.

If you discontinue the policy, the amount you will get is called the special surrender value. This is arrived at by multiplying the total paid-up value (paid-up value + bonus) with a multiplier called the surrender value factor.

The surrender value factor is a percentage of paid-up value plus bonus. It is zero for the first three years and keeps rising from thirdyear onwards. It differs from company to company and depends on various factors.

"Different companies use different approaches to arrive at the surrender value factor. Usually, the calculation takes into consideration factors such as completed policy years, policy type and time to maturity, with-profit fund performance in case of participating policies, besides the company's customer philosophy and industry practice," says Suresh Agarwal, executive vice-president, head, distribution and strategic initiatives, Kotak Mahindra Old Mutual Life Insurance.

Not all companies declare the surrender value factor in the product brochure or on their website.

"This information can be obtained from the agent or the insurance company directly," says Rajeev Kumar, chief and appointed actuary, Bharti AXA Life Insurance. The special surrender value calculated in the box above is what you get against Rs 75,000 premium paid if you surrender the policy after three years.

TO SURRENDER OR NOT? Surrendering an endowment policy makes sense only if the amount (surrender value) received on doing so and invested in another product can generate a better return than the policy would have on completion of tenure.

"We usually do not recommend surrendering a policy as the customer not only loses out all the benefits of the insurance scheme but also receives a much lower amount than the total premium he must have paid," says Rajeev Kumar of Bharti AXA Life Insurance.

If you plan to dump your endowment policy, bear in mind all the money you have paid that you may never get back.

Government has decided to make it compulsory for every individual to link their Aadhaar Card with PAN card by 31st July, 2017. This is part of the digital India campaign and an attempt to digitalize everything.

Why it is mandatory to link Aadhaar with PAN?

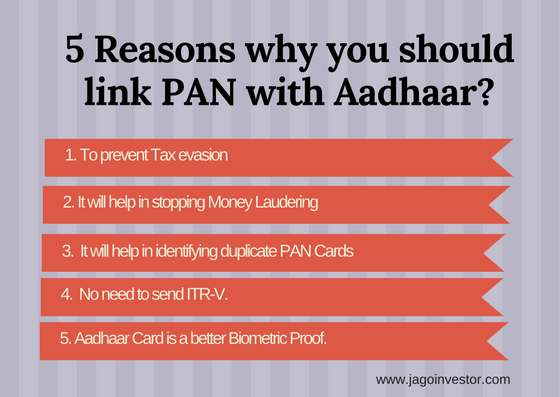

There is a great chance that there are a lot of fake PAN cards in India, because it can be easily applied online with fake identities and anyone with a little luck can get a duplicate PAN card. Hence in order to identify those fake PAN cards, govt wants to link Aadhaar card with PAN.

Because each person will have only one Aadhaar card, they will only be able to link it with a single PAN. Rest other PAN cards will be of no use after this process. This is an important move and is necessary for an orderly society and also to keep pace with the technology.

Importance of linking Aadhaar with PAN

PAN card and aadhaar card are the unique identification cards which can be used for verifying a person’s income and address respectively. Let’s have a quick view why this linking is important.

Some reasons behind linking aadhaar with PAN in details are as below:

Fraud PAN cards– Because of this linking a person can use only one PAN card wherever it is necessary which is linked with his aadhaar card. Though he has any fraud/duplicate PAN card, it will be of no use.

Tax Evasion – with the help of this, government will be able to track on the taxable transactions of an individual or an entity.

Tracing money launders- Aadhaar card is a full-proof identification of an individual and it cannot be duplicated easily so that linking of aadhaar with PAN can also be useful for tracing money launders.

There are fewer chances to have a duplicate aadhaar card as it is a more secured source of identification. Because Aadhaar card is the only identity proof which has all the possible information including Bio-metric. So it is little bit difficult to have a fake aadhaar card as compared to PAN Card and voter ID.

Curb corruption: This is also useful to curb corruption to a significant level as the record of each transaction will be verified by the government.

Also, the government wants to get every individual identified by their Name, Address and also their income. A lot of PAN cards were very old, and many people have changed their address, contact details etc which were given to govt at the time of applying for the PAN card decades earlier. With this linking, all the data will also get updated.

What is the process to link aadhaar card with PAN?

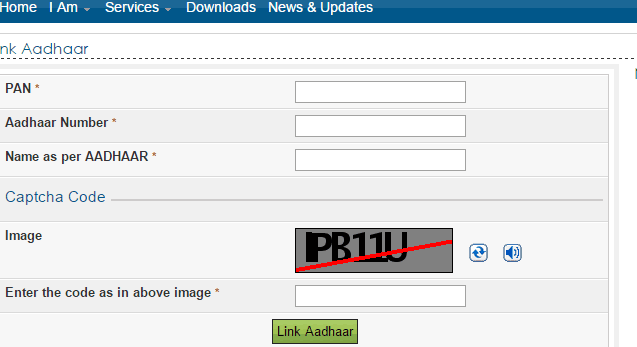

If you are unable to link your aadhaar card with PAN, no need to worry. Here are the steps to link your aadhaar card with PAN.

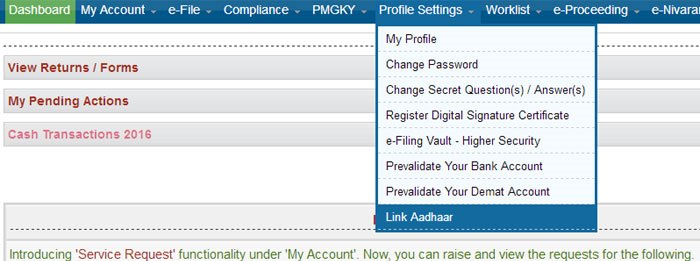

Visit the page of Income tax e-filling portal & register if you are not registered with it. If you have your registration already then just login.

Login with the details i.e. registration ID, Password or date of birth.

Your PAN no. will be your registration ID

once you login you will immediately get a pop-up to link your aadhaar with PAN

If you don’t get a pop message then check the blue bar above and click on “Profile setting” and then on “Link aadhaar” in the list.

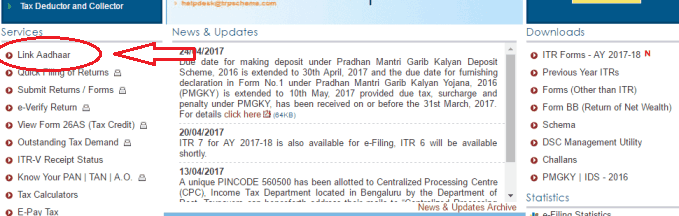

Or you can also see the option “Link Aadhaar” on the left side of the site when you open it without logging in. Simply click on it.

The details like your name, gender and date of birth will be given there already as per the registration. Just check that the details available there are same as on your aadhaar Card.

If the details match with aadhaar card then fill your aadhaar card number and captcha code and click on “Link Aadhaar”.

Once you submit you will get a pop-up that your aadhaar has been linked with your PAN successfully.

What happens in case of name mismatch between Aadhaar and PAN?

UPDATE:Now you can link your aadhaar card with PAN without changing your name as the option “Name on Aadhaar” has given there.

Now it’s suggested that you first decide what is the exact name you want to keep for future, in case you have different names on various documents.

If your aadhaar card has the name which you want to keep, then you should change your name in PAN. However if your PAN has the desired name, then change it in Aadhaar card.

Now, for those who want to change their name in aadhaar card, they can follow this process or watch the video below.

We really feel that one should have the proper name in Aadhaar card, because it’s going to be the universal documents in future.

UPDATE: New Feature by IT department

Besides this, there is also a new option on the e-filling site from where you can link you Aadhaar card with you PAN card without changing your name.

Only date of birth, Name and Gender on both the documents should match, however we feel that as a long term solutions it’s a good idea to have the same name on both the documents.

What to do if I don’t have one of the documents (Either PAN or Aadhaar)

Now a days, almost all the people at least in urban areas have both aadhaar and PAN, very rarely it happens that someone does not have both the documents. However incase one of the documents is missing, here is what you should do ..

For those who do not have PAN

If you don’t have PAN card, then this rule is not applicable to you right now. You don’t need to take any action at the moment.

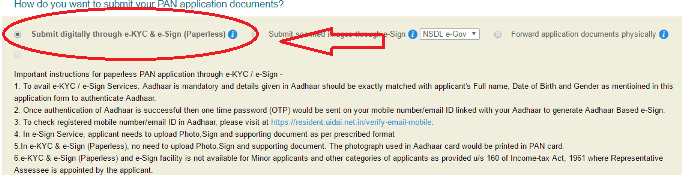

When you apply for PAN in future, at that time you can give your Aadhaar details as the address proof while applying for PAN offline or you can choose an option called digital e-kyc and e-sign, where you will be asked for aadhaar number and it will be automatically linked to your PAN. Below is a snapshot of the e-KYC looks like.

What do you if you don’t have Aadhaar?

If you don’t have Aadhaar card then you should apply for it soon, because anyways it’s going to be the universal mandatory documents very soon and every PAN has to be anyways linked with aadhaar. You can apply for aadhaar card by online or by visiting its office and providing you essential documents.

How to Check whether your PAN card is linked with Aadhaar card or not?

For some people their PAN might be already linked with Aadhaar card. To check this you just have to visit the official page of e-filling and click on the login button on the right corner of the site. Fill your PAN number and captcha code and click on OK.

If your card is already linked then it will show “Your Aadhaar is already linked with PAN” and if your card is not linked then it will show “User ID does not exist”.

Below is the demo of this process

Is it safe to link your PAN details with Aadhaar?

Recently there was a news that M. S. Dhoni’s Aadhaar details were leaked somehow, which shows that aadhaar details are not 100% secured. If this can happen to a big celebrity, this can happen to anyone.

Many people are wondering if it’s safe to link their Aadhaar with their PAN?

Will their bank details be exposed ?

Will there be any fraud involved?

Will others get access to their income tax data ?

Will others get access to my personal data like Mobile number, Email and Bio-metric details?

But, you don’t need to worry!

The solution to problem is here. There is no need to worry about the security of your PAN after linking with Aadhaar. UIDAI has introduced safety features of aadhaar Card.

Now there is a facility of “Lock” and “Unlock” of aadhaar details.

If you “Lock” your aadhaar details, all your data will be freezed and the access to any third party will be blocked. All you will need to do is, verify the OTP which is sent to you when you apply for this “Lock” feature online. If you want to get details about all the safety features, you can download this PDF.

What will happen if your Aadhaar card is not linked with PAN card?

As per this amendment if a person do not link his aadhaar with PAN card then there is possibility that he could lose his access to the PAN card after December 31,2017 as per Hindustan Times.

You will be unable to file IT returns and pay the dues or claim the IT returns.

It’s been also said that the use of PAN cards may stop in upcoming days as Aadhaar card will be the unique Identity proof. So if you don’t link it now you have to link it with your PAN in future in any ways.

Because your PAN card will be blocked, and for higher value transactions PAN is mandatory, you will not be able to do many high value transactions online as the bank will keep asking for PAN

UPDATE:What if I have both the documents but don’t have any Income Tax Returns?

If you don’t file any Income Tax Return then this rule is not for you. It will not affect either you link your Aadhaar card with PAN or not.

But if you have both the documents, we suggest to link the documents.

UPDATE: What if I’m an NRI and have only PAN card?

If you are NRI and earning in India then you also need to file Income Tax Return. For that you need Aadhaar card.

NRI’s can also apply for the Aadhaar card. The procedure and documents required for NRI and Foreigners are same as Indian residential’s. Only thing is they have to be physically present at any of the Aadhaar card center in India.

How can I apply for Aadhaar if I’m out of India?

If you are not in India currently and wanted to apply for Aadhar crad then the procedure is almost same. But you should have an introducer who can introduce you by providing his/her own Aadhaar card.

The verification of your identity will then become the responsibility of the introducer.

So, what are you waiting for ?

You should quickly complete this whole process as it’s just a 5-10 min work. Not completing this can impact you in negative way, so do not wait for the last minute.

Also you should spread this news among your friends and help others to complete this important step in their financial life.

In case you have any questions, I will be happy to answer them in comments section

Young investors have an edge over others on account of their age. In other words, a young investor has more time on hand as compared to middle-aged investor or one who is nearing retirement. Young investor can take higher risk compared to middle aged investor or nearing retirement investor. This in turn affords young investors greater flexibility while making investment decisions.

Young investors have an edge over others on account of their age. In other words, a young investor has more time on hand as compared to middle-aged investor or one who is nearing retirement. Young investor can take higher risk compared to middle aged investor or nearing retirement investor. This in turn affords young investors greater flexibility while making investment decisions.

There are various investment avenues available to young investors and the various facets of each avenue like small saving schemes, equity, mutual funds, ELSS, unit linked insurance plan, etc. Today youth should ensure that he is associated with the right investment advisor at all times. He could well be the individual who plugs the gap between youth achieving or not achieving his financial goals and objectives. Financial markets have become very complex and there are varieties of products available to choose from. The choice of product will depend upon:

There are various investment avenues available to young investors and the various facets of each avenue like small saving schemes, equity, mutual funds, ELSS, unit linked insurance plan, etc. Today youth should ensure that he is associated with the right investment advisor at all times. He could well be the individual who plugs the gap between youth achieving or not achieving his financial goals and objectives. Financial markets have become very complex and there are varieties of products available to choose from. The choice of product will depend upon: